UNIT 1

UNIT 1

Synopsis:

1.cost accounting - introduction, objectives, functions, cost sheet, cost concepts, classification2. Management accounting - Nature, scope, functions

3. distinguish between financial accounting, cost accounting, and management accounting

4.methods of costing - job, batch costing

Example: Advertisement, salesmen salaries, brokerage and commission, bad debts, showroom expenses, traveling expenses:

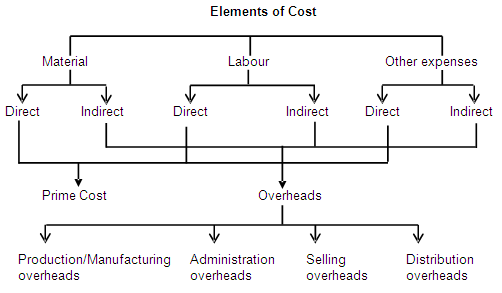

A cost sheet is a document that provides for the assembly of the estimated detailed cost in respect of a cost center or a cost unit. It is a detailed statement of the elements of cost arranged in a logical order under different heads. It is prepared to show the detailed cost of the output for a certain period. It is only a memorandum statement and does not form part of the double-entry system. Additional columns can be provided to indicate the cost per unit at different stages of production or to enable a comparison to be made of the current costs with that of historical costs.

The main advantages of a cost sheet are:

- it indicates the break-up of the total cost by elements, i.e. material, labour, overheads, etc.

- it discloses the total cost and cost per unit of the units produced

- it facilitates comparison

- it helps the management in fixing selling prices

- it acts as a guide to the management and helps in formulating production policy

- it enables keeping control over the cost of production

- it helps the management in submitting quotations or preparing estimates for tenders

- it is a simple and useful medium of communication of costs to various levels of management.

Job costing involves a considerable amount of recording & analysis. It requires reliable production control records which must show material issued to various jobs, labor time spent on different jobs & appropriate allocation of overheads. Each job passes through production cost centers. A separate job cost sheet is maintained for each job/product in which all expenses of material, labor, & overhead are recorded. The cost of completing a job /manufacturing a product is found out.

Nature & suitability of job costing :

Many organizations manufacture products / provide services on receipt of a specific order from a customer as per his requirements. In such a case, no two jobs are necessarily alike & they don't pass through the same manufacturing process. Different jobs require a different amount of material, labor, and skills. Thus, job costing is used when products/ services are dissimilar.

The distinguishing features of a situation where the job costing method is applied are as follows:

1. The job is undertaken for a specific customer & not for mass production.

2. Each job is unique. It has its own characteristics & needs special treatment. No two jobs are necessarily alike.

3. Each job doesn't pass through the same manufacturing process. The nature of the job determines the departments through which the job has been produced.

4. Cost can be identified with a specific job/order.

5. The job can be identified at each stage of production, from start to completion of the job.

6. The work-in-progress differs from time to time depending upon the no.of jobs on hand.

7. The time required to complete a job is comparatively short compared to a contract.

Thus, job costing is generally used in the following types of industries :

(a) printing, where each print requires a specific type of paper, ink, design

(b)Furniture, where it is manufactured as per the specific requirements of a customer.

(c)Repair works

(d)shipbuilders,

(e)Interior decoration, advertising, and other professional services, where each job needs special treatment.

Objectives :

The following are the main objectives of job costing.

1. To ascertain the cost of each individual job/order.

2. To determine the profit /loss of each job.

3. To help the management in the valuation of work-in-progress.

4. To help in the estimation of the cost of an order / a job so as to quote a price to the prospective customer.

5. To serve as a tool of cost control by comparing the actual cost with the estimated cost.

Advantages: The advantages of job costing are as follows:

1. It helps in ascertaining the cost of each job separately.

2. It provides a detailed analysis of various elements of cost which enables management to identify inefficiencies in operations.

3. It helps to distinguish profitable jobs from unprofitable jobs.

4. It helps in the valuation of uncompleted jobs.

5. Wastage, spoilage & defective work can be reported for specific jobs enabling the management to take corrective action.

Batch costing is a method of costing that is used in industries where production is carried out in batches. It is generally applied in pharmaceutical industries, snack food industries, toys manufacturing industries, and spare parts manufacturing industries.

Meaning:

Batch costing is a type of specific order costing where articles are manufactured in predetermined lots, known as a batch. This method is used to ascertain the cost & profit of specific batches/ units in a specific batch.

Features:

- Each batch is treated as a cost unit

- All costs are accumulated & ascertained for each batch

- A separate batch cost sheet is used for each batch & is assigned a certain number by which the batch is identified

- The cost per unit is ascertained by dividing the total cost of a batch by the number of items produced in that batch.

Economic batch quantity: Economic batch quantity (EBQ)refers to the optimum quantity batch which should be produced at a point in time so that the setup & processing costs & carrying costs are together optimized.

Formula: √2AS÷C

Whereas, A= Annual demand S= Set up the cost per batch C= Carrying cost per unit per year

Q) DIFFERENCES BETWEEN JOB & BATCH COSTING:

BASIS FOR COMPARISON

JOB COSTING

BATCH COSTING

Meaning

Job costing refers to a specific costing method, used when the

production/work is carried out according to the requirements of customers

Batch costing is a form of job costing, that is applied when

the articles are produced in batches, i.e. a group of like units are produced

Production

As per customer specification

Mass production

Product

Products have an independent identity, as each job is distinct

from other jobs

Products do not lose their individual identity, as they are

manufactured in a continuum

Cost unit

Executed Job

Batch

Cost ascertainment

On the completion of each job

Ascertained for the

whole batch and then per unit cost is determined

5Q) COST CONCEPTS:

cost: The amount of expenditure incurred on / attributable to a specified thing / activity.

costs may be classified on the basis of decision making purposes for which they are put to use in the following ways:

- fixed cost

- variable cost

- historical cost

- replacement cost

- opportunity cost

- out of pocket cost

- sunk cost

- incremental cost

- marginal cost

1. fixed cost: costs which remain fixed and not change in proportion to the volume of output are known as fixed cost.Example: Rent , insurance of factory building etc. remain the same for different levels of production.

2. variable cost: cost which change in direct proportion to the volume of output are known as variable cost.Example: cost of direct material, direct labour etc.

3. historical cost: historical cost is the original cost of an asset, as recorded in an entity's accounting records. Many of the transactions recorded in an organisation's accounting records are stated at their historical cost. According to the accounting standards, historical costs require some adjustment as time passes. Depreciation expense is recorded for long term assets, there by reducing their recorded value over their estimated useful lives.

4. Replacement cost: It is the price that an entity would pay to replace an existing asset at current market prices with a similar asset.

5. Opportunity cost: It is the value of the benefit sacrificed in favor of choosing a particular alternative . It is the cost of the best alternative foregone. If an owned building, for example , is proposed to be used for a new project, the likely revenue which the building could fetch, when rented out, is the opportunity cost. It should be considered while evaluating the profitability of the project.

6. Out-Of-Pocket Cost: It is the cost which involves current / future expenditure / out lay , based on managerial decisions. For Example, a company has its own trucks of transporting goods from one place to another. It seeks to replace these by employing public carriers of goods. while making this decision management can ignore depreciation, but not the out of pocket cost in the present situation, i.e. fuel, salary to drivers and maintenance paid in cash.

7. sunk cost: A sunk cost refers to money that has already been spent and cannot be recovered. A manufacturing firm, for example, may have a number of sunk costs. Such as the cost of machinery, equipment and the lease expense on the factory.

8. Incremental cost: The incremental costs are the additions to costs resulting from a change in the nature and level of business activity.Example: Changing the product line/ changing the level of product output. buying additional / new materials, Hiring extra labour, adding new machines or replacing existing ones.

9. Marginal cost: The amount of any given volume of output by which aggregate costs are changed if the volume of output is increased by one unit.Example: the cost of production of 1000 units of radios is Rs. 2 lakhs and that of 1001 units is Rs. 200150 the marginal cost is Rs. 150(i.e. Rs.200150-200000)

6Q) Management accounting - Nature, scope, functions(10M)

BASIS FOR COMPARISON

JOB COSTING

BATCH COSTING

Meaning

Job costing refers to a specific costing method, used when the

production/work is carried out according to the requirements of customers

Batch costing is a form of job costing, that is applied when

the articles are produced in batches, i.e. a group of like units are produced

Production

As per customer specification

Mass production

Product

Products have an independent identity, as each job is distinct

from other jobs

Products do not lose their individual identity, as they are

manufactured in a continuum

Cost unit

Executed Job

Batch

Cost ascertainment

On the completion of each job

Ascertained for the

whole batch and then per unit cost is determined

- providing accounting information

- cause and effect analysis

- use of special techniques and concepts

- taking important decisions

- achieving of objectives

- no fixed norms followed

- increase in efficiency

- supplies information and not decisions

- concerned with forecasting

- financial accounting

- cost accounting

- financial management

- budget and forecasting

- inventory control

- reporting to management

- interpretation of data

- control procedures and methods

- internal audit

- tax accounting

- planning and forecasting

- modification of data

- financial analysis and interpretation

- facilitates managerial control

- communication

- use of qualitative information

- co ordinating

- helpful in taking strategic decisions

- supplying information to various levels of management

Comments

Post a Comment